There are two things that can be said for certain about spare parts (including miscellaneous maintenance materials) –

- Stocking them is expensive and

- Not stocking them is expensive.

This article explores the components of the cost of stocking and of not stocking parts and suggests a rational approach to keep the total of these costs to a minimum.

Deciding what parts to add to, or keep in stock is often emotional (“I’ve been burned before..”) or illogical. An example of an illogical decision is to remove all items from stock that have not moved in, say, ten years. This is the equivalent of removing all fire extinguishers that have not been used to fight a fire for ten years – at least it will be for some of the items that will be removed from stock.

There is a logical process for deciding what parts and other maintenance materials to keep in stock. While the process described here is rational, it is also somewhat complex and applies to each component individually, and it also depends on the way in which each component may fail – its “failure mode”.

As an example of failure modes, consider a car tire. Two (of several) modes of failure are “normal wear” and a “puncture”. A puncture can occur without warning and it makes little difference if the tire is new or old. For the “puncture” mode of failure, it makes sense to keep one spare “in stock”. On the other hand, normal wear occurs slowly and predictably, so with routine inspections worn tires can be replaced before they “fail” (by becoming dangerous) so there is no need to keep spares for this “normal wear” mode of failure. This simple example of the importance of routine inspections to detect failures in time to prevent breakdowns leads us to a very important principle:

An effective preventive maintenance programme can greatly reduce the need to keep an inventory of many spare parts.

Unfortunately, in most organizations the responsibilities for managing the preventive maintenance programme and for looking after the Storeroom are quite separate, perhaps even under different managers, so this principle is frequently not given the consideration it deserves.

We’ll come back to the logic behind making spare parts decisions, but first let’s look at the components of the two major costs related to Maintenance storerooms.

- The cost of stocking spare parts includes:

– purchasing parts before they are needed in the operation, and financing of these early purchases

– protection, including buildings, heating and air quality

– organization, including racks and bins, and labour for stocking and retrieving parts, for administering receipts and issues and for general housekeeping and reporting

– wastage, including the disposal of perishable materials which have reached their “best before” date, unauthorized removal, damage, etc

– supporting costs, such as payroll, janitorial, IT, etc.

- The cost of not stocking spare parts includes:

– lost production in the event of a breakdown

– reduced maintenance effectiveness on work which is not planned in great detail (i.e. most routine maintenance work)

– reduced reliability from using incorrect or makeshift parts

– the additional cost of processing purchase orders, shipping, receipts and invoice payments which could be avoided if parts were in inventory, when several would be ordered at one time.

The cost of stocking and of not stocking spare parts are real costs and the sum of these two costs should be minimized. Unfortunately, each of the components of the cost of stocking parts is relatively easy to measure, while the components of the costs of not stocking parts are difficult to measure. It is important to avoid the temptation to place too much emphasis on reducing the easy-to-measure costs and to ignore the very hard-to-measure results.

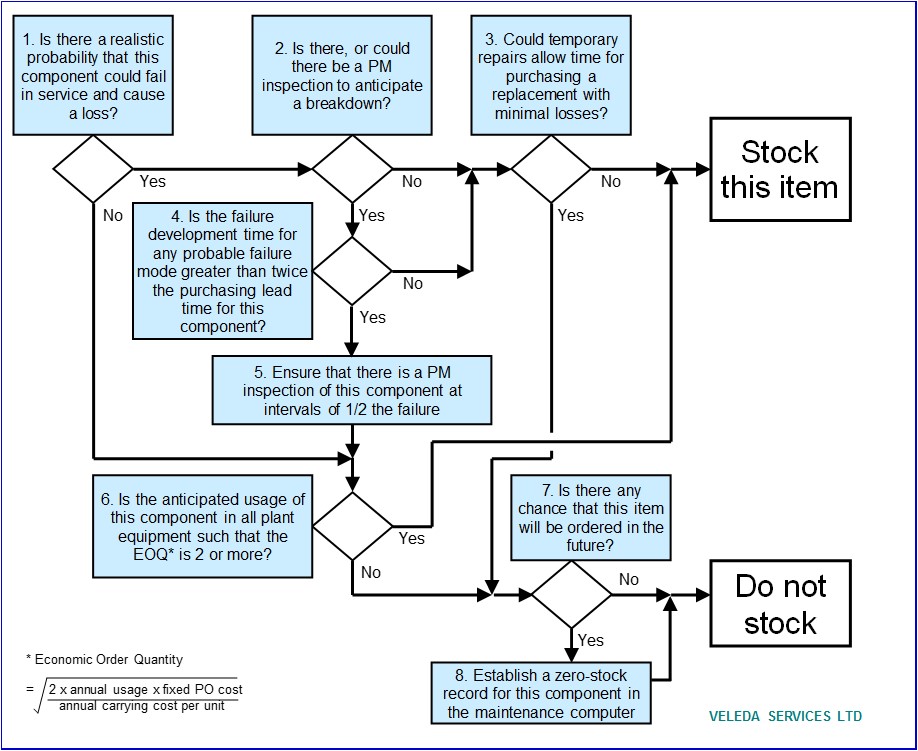

Deciding what parts to stock is not simple, but it should be logical as illustrated in the diagram below. Most of the remainder of this article will look in some detail at each of the boxes in this diagram.

- “Is there a realistic probability that this component could fail in service and cause a loss?”.

Note that this question considers “components” and not “equipment”. It is components that fail, but spare parts are not always just components, they may be assemblies or complete equipment units, depending on the effort and time required to replace them in the operation. In this article, “components” refer to the unit that it is logical to replace.

This decision on the “realistic probability of a loss” should be made by an expert who understands both the component and its “operating context” (imposed loads, operating environment, etc). Most components of equipment will last the life of the equipment itself. The items which should be considered for inventory include wearing parts (brake linings, parts in contact with the process, etc), sacrificial protective equipment (fuses, shear pins, etc) and parts which experience with similar components in similar service has shown that they may fail.

Recent improvements in manufacturing techniques, supported by such systems as ISO 9000, have greatly increased the reliability of many common equipment components. This change has reduced the need to stock some components which may routinely have been kept on hand in the past.

If “Yes” – go to 2

If “No” – go to 6

- “Is there, or could there be a PM inspection to anticipate a breakdown?”

This inspection could be anything from a simple visual inspection to any non-destructive test (vibration analysis, ultrasonic thickness measurement, etc).

If “Yes” – go to 4

If “No” – go to 3

- “Could temporary repairs allow time for purchasing a replacement with minimal losses?”

An example is a large ring gear on a ball mill (pictured below). One mode of failure is for a tooth to crack or break off, which may happen rapidly. If a repair method can be developed, then it will buy the time needed to order a replacement.

It is a good practice to consider these possibilities, develop a repair procedure and keep it in the equipment file so that in the event of a failure the component can be returned to service in the shortest possible time (see “Reducing the risk of unspared critical components“).

If “Yes” – go to 7

If “No” – Add this item to stock

- “Is the failure development time for any probable failure mode greater than twice the purchasing lead time for this component?”

The “failure development time” (FDT) is the elapsed time from when a failure can first be detected to the time of breakdown, i.e. when the component can no longer perform its required function. For some components, such as tires or conveyor chains, the FDT for normal wear is the life of the component – wear starts as soon as it is put into service. For other components, such as fuses, the FDT may be milliseconds. For many components, such as bearings, there are many possible modes of failure and the FDT is very dependent on the type of inspection and the experience of the inspectors, whoever they may be. For more on FDT, an excellent reference is “RCM II”, by John Moubray.

If the FDT is more than twice the purchasing lead time, then inspecting the component at a frequency of 1/2 the FDT will provide enough time to purchase a replacement prior to a breakdown, and therefore a spare does not need to be stocked.

NOTE – Lead times can be a problem, especially for slow-moving spares for older equipment. At the time the equipment was purchased, spares may have been stocked by a local distributor with same- or next-day delivery. With the ongoing pressure to reduce inventories at all steps of the supply chain, when a spare is finally needed, it may have to come from a national distribution centre, or even the manufacturer. In some cases, it may have to be made before delivery. The resulting increases in lead times, which can be dramatic, will result in the need to add components to stock, and staying on top of these changes is a considerable challenge.

If “Yes” – go to 5

If “No” – go to 3

- Ensure that there is a PM inspection of this component at intervals of 1/2 the FDT”

This is vital! The photograph below shows a section of a storeroom rack containing many hundreds of thousands of dollars worth of chain and conveyor drive sprockets. These share two characteristics – their only known failure mode is normal tooth wear, and they are all very easy to inspect in service. There should be no need to keep any of these sprockets in stock, and it is most likely that the reason they are there is that the PM inspection programme is not trusted (although there is another possible reason – see 6. below).

If the PM programme is well-designed and followed with discipline, the start of failure of components, such as these sprockets, with a long FDT will be identified in time to purchase and install replacements before a breakdown occurs and they do not need to be stocked.

This relationship between the PM inspection programme and spare parts inventory is one reason (of several) for the Stores and Maintenance to share a common technical management.

- “Is the anticipated usage of this component in all plant equipment such that the EOQ is 2 or more?”.

Economic Order Quantity (EOQ) is the re-order quantity that minimizes the sum of the cost of processing orders plus the carrying cost. The formula is:

This is a simple formula, in fact some maintenance computer systems will calculate the EOQ based on usage history, with the fixed PO cost and annual carrying cost entered, usually manually.

However, EOQ calculations are not as simple as this suggests. Looking at each of the terms in the formula:

– “annual usage (units)”. If historical usage is used, the formula will be unreliable if large issues have been made for projects, major shutdowns, etc. The annual usage should be for normal, ongoing maintenance needs and should be reviewed by a knowledgeable person to ensure that it is realistic.

– “fixed purchase order (PO) cost”. This is the cost of processing a purchase order that is independent of the number of units ordered. The components of the fixed PO cost include:

– the cost of entering a purchase order, which may include obtaining quotes.

– the cost of processing the receiving documents.

– the cost of paying the invoice.

– other costs, as discussed below

It may include none, all or some of the freight cost, depending on the way in which freight is arranged. And there may be “step” changes in freight costs which complicate the calculation. For example, up to 50 boxes may require one truck, but 51 boxes will require two trucks.

It may also include some or all of the cost of handling and binning the items when received.

The fixed PO cost may include other, significant, items. In the case of the sprockets in the photo, if these are custom sprockets, there may be a tooling, or setup charge for the first sprocket, and then a much smaller cost for other sprockets using the same tool setup. This setup cost should be included in the “fixed PO cost” for the EOQ calculation. If that is the case, then keeping these sprockets in stock may become economic, not to minimize losses when they “unexpectedly” wear out but to minimize inventory costs.

The fixed PO cost may be reduced by combining several SKU’s on the same replenishment PO to a vendor (e.g. by using a “dual re-order point” system).

– “annual carrying cost per unit”. This includes financing costs and the cost of facilities, energy and labour required to store, protect and handle the component. The calculation of this cost may be somewhat complex, and it has been quoted as between 15% and 30% of purchase price. It is plant-specific and it is a number that is worth calculating. Bear in mind that prices may also have quantity break points which further complicate the calculation.

While the EOQ is an important number, taking the above factors in to account makes the calculation less than precise. The important thing is to know that there is an economic quantity to order, and some examples of EOQ for common stock items will provide guidance to Storeroom and Purchasing staff.

Of course, it makes no sense to order the exact quantity based on EOQ calculations. For example, if the EOQ calculation shows that the reorder quantity for 6 volt batteries is 78, but they are packaged in boxes of 50, then the sensible order quantity will be one or two boxes. This may not seem very precise, but it does show that the reorder quantity should not be 10 boxes, and the square root function in the calculation reduces the sensitivity of the overall cost to the order quantity.

If “Yes” – stock this component

If “No” – go to 7

- “Is there any chance that this item will be ordered in the future?”

This includes large, long life components, such as pump volutes, gear casings, etc that are not economical to stock, based on the above logic. Where a manufacturer has supplied a list of all components for an item of equipment, most of these items should be considered as possible future purchases.

If “Yes” – go to 8

If “No” – do not stock this item

- “Establish a zero-stock record for this component in the maintenance computer”

Components that should not be stocked, based on the above logic, but which may be required some time in the future, should be included in the Storeroom SKU catalogue, with no stock. The sprockets in the above photo are a good example. Adding these to the catalogue makes “ordering on request” very simple, because all ordering information, including the vendor, is easy to access for the Planner or whoever orders the item. It also tracks history so if usage increases, an EOQ can be calculated to determine if keeping the item in stock has become economic.

The inclusion of non-stock items in the SKU catalogue is an extremely powerful tool. For further details see “The power of the ‘zero-stock’ catalogue“.

How many of each component should be stocked?

Again, this is something that should be determined by an expert who is familiar with the component and its use. It should be based on sound logic. An arbitrary decision to reduce inventory by reducing the re-order or safety stock levels for all SKU’s to one (it has been done) will almost certainly increase operating losses.

As an example of stock quantity, consider fuses for a typical 3-phase industrial branch circuit. It is good practice to replace all three fuses if one fails, so the absolute minimum safety stock is 3. When a fuse fails, if the cause is not obvious while the equipment is down, then the next troubleshooting step is normally to replace the fuses and start to power the equipment up. This may result in another fuse failing, so to cover this possibility, the minimum safety stock should be increased to 6 – or more. All components should be subject to this kind of technical assessment when setting quantities. Of course, the EOQ may be greater than the quantity dictated by this technical evaluation.

Use of the Storeroom for projects

Most inventory-reduction efforts focus on removing SKU’s that are considered uneconomic to stock, because of low turnover or other reasons. My observation is that there is often a larger opportunity in reducing the safety stock and reorder quantity of many SKU’s, because they have been set up to provide materials for projects. For example, in one large paper mill a bin contained 12 6″ schedule 40 316 stainless steel elbows. For maintenance purposes, these have a very long service life and no one could remember an occasion when more than one was needed at a time for maintenance. This storeroom was being used as a project storeroom.

Maintenance storerooms should be just that – for maintenance needs only. Project materials should be purchased for each project as needed, although the stock replenishment process (contract vendor, etc) should be used where possible. Surplus project materials should be returned to the vendor or, if they duplicate a stock item and are likely to be used in a reasonable time, returned to the Storeroom overstock system.

One last word on maintenance inventory reduction. Canadian accounting practice dictates that stock items which are stored as working capital must be expensed when they are withdrawn, even if it is for disposal. If these parts are expensed against the Maintenance budget (not uncommon), there will be little enthusiasm to remove items from stock at all because:

– the Maintenance Manager will probably have to assign his best people for a considerable time to determine if parts are safe to remove from stock

– the process of removing the parts may put his/her department over budget.

– there are always more important things to be done.

The accounting system must ensure that Maintenance is not penalized for doing the “right thing” by keeping Storeroom inventory at a optimum level (see “Optimum Maintenance“)

Click here to return to the articles list

Management is getting people to do what you want them to do.

Leadership is getting people to want to do what you want them to do (dsa).

© Veleda Services

Don Armstrong, P. Eng (retired)

President, Veleda Services

dsarmstrong@shaw.ca

250-655-8267 Pacific Time